How Banks Can Slash Loan Processing Times with DeepQ: The Agentic AI Solution for Faster, Smarter Underwriting

In today’s banking landscape, speed and accuracy are critical competitive differentiators. Customers expect quick decisions. Regulators demand rigorous compliance. Yet for many banks, the loan application review and underwriting process remains burdened by paperwork, delays, and manual errors. This undermines customer satisfaction, increases operational costs, and slows growth.

That’s where DeepQ comes in. By marrying the capabilities of Knowledge Agentic AI with enterprise-grade features, DeepQ promises to streamline loan approvals, reduce risk, and deliver faster, more reliable decisions.

The Loan Processing Challenge: Why It’s So Slow

To understand why DeepQ matters, it helps to see how loan processing typically works, and where the bottlenecks are.

Typical Process & Time Spent:

- Large volume of documents: Loan Officers, Credit Analysts, and Underwriters must review a large volume of documents: financial statements, tax returns, bank statements, employment verification, credit reports, collateral/appraisal documents, regulatory compliance paperwork. Each file may contain 50-200 pages scattered across multiple systems.

- Tedious Manual Effort: Staff spend 10-15 hours per application just reading, verifying, cross-referencing, and manually flagging potential issues. For complex commercial loans, this workload can easily expand to 30-40 hours of document review, significantly straining resources.

Pain Points

- Cumbersome Paperwork & Fragmented Data: Documents may come in various formats(PDFs, scans, spreadsheets..etc), and be stored in different systems or siloed departments. Locating, retrieving, and synthesizing all necessary information is time-consuming.

- Manual Verification & Cross-Referencing: Staff manually check financial statements against bank statements, employment income matches tax returns, past credit obligations are correctly disclosed, collateral appraisals are consistent, etc. This introduces risk of human error and often causes delays when discrepancies are found.

- Regulatory & Compliance Burden: Ensuring all regulatory requirements (e.g. KYC, AML, internal risk policies, exposure limits) are satisfied, and often requires cross-department audit or compliance review.

A DeepQ Use Case Flow: Underwriting a Commercial Loan

Here’s how a loan officer / underwriter will use DeepQ in practice, end-to-end, to shorten time and raise confidence:

- Document Verification: Loan officer collects all the documents, and uploads into the DeepQ platform, and triggers the document verifier to ensure that all the required documents are in order.

- Knowledge Update: DeepQ processes the uploaded documents after successfully verified, and updates the underlying knowledge bank.

- Automated Initial Assessment: DeepQ automatically extracts key information such as income, liabilities, credit score, collateral value from the knowledge base. It cross references the details, and highlights the data inconsistency and integrity issues across the sources.

- Compliance & Risk Checks: DeepQ checks the state of the loan request against the bank’s compliance and regulatory rules, and internal risk thresholds. The platform identifies and flags the discrepancies if any.

- Further Clarifications: Underwriters can query the system conversationally. For example, an underwriter can ask “Show me any discrepancy between the declared income and bank deposit trends over the last 6 months”.

- Decision Summary: DeepQ generates a risk-assessment summary that includes key metrics, red flags, compliance status, decision suggestion (approve / decline / need more info), all in a concise report. The responsible officers in the loan approval line will review the summary of the loan assessment and make a decision.

- Post Decision Action Plan: Depending on the decision, the subsequent communications will be triggered to the borrower. Eg, if the loan is approved, relevant approval documents will be generated, communication will be sent to the borrower and funds will be deposited.

The net result: what might have taken a week or more can happen in hours (for many loans), with much less human bandwidth.

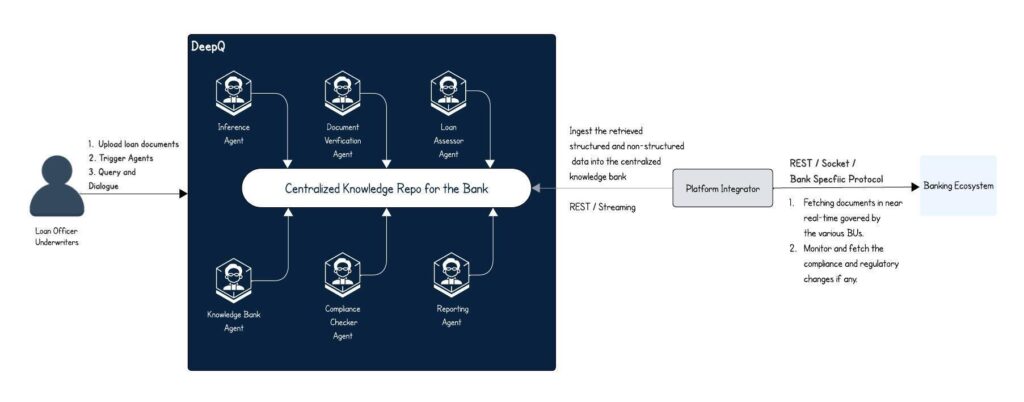

The diagram below shows the high level design of the application.

- Document Verifier Agent: Automatically validates uploaded documents for completeness, consistency, and authenticity.

- Knowledge Bank Agent: Indexes verified documents into DeepQ’s centralized Knowledge Bank for intelligent retrieval and reasoning.

- Loan Assessor Agent: Analyzes applicant financials, generates preliminary credit assessments, and provides detailed decision insights to underwriters.

- Compliance Checker Agent: Evaluates each application against internal policies and regulatory frameworks to flag compliance and risk concerns.

- Reporting Agent: Generates final approval or rejection documents and prepares structured outputs for audit and downstream processing.

- Inference Agent: Generates deep context aware responses for the queries from the users, having a realistic and human nature dialogue with the them.

The Benefits: Numbers & Outcomes

Here are the key benefits banks can expect when deploying DeepQ for loan application review and underwriting:

- Massive Time Savings: DeepQ can cut review and cross-referencing hours by 70-80%. What would take 4-8 hours manually can become something like 1 hour or less. Complex commercial loans that might take 15-20 hours to process manually can be dramatically shortened.

- Decision Speed: For simpler loans or loans where data is readily available, DeepQ makes same-day decisions feasible. The “days or weeks” timeline becomes “hours”.

- Higher Accuracy with Lower Risk: Automatic flagging of missing or inconsistent documents, detection of stale data, cross-document checking reduces human error. This improves risk assessment and reduces downstream problems.

- Improved Customer Satisfaction: Faster turnaround, fewer requests for follow-ups or clarifications, clearer communication, more transparency. Loan seekers are more likely to choose institutions that move quickly.

- Compliance with Confidence: DeepQ monitors and updates the compliance and regulatory framework changes in near real-time, every loan application will pass through the up-to-date compliance and regulatory checks.

What are the Strengths of DeepQ?

DeepQ is built from the ground up to address these pain points. Here’s a breakdown of how its features map to what loan officers, credit analysts, and underwriters need.

| Feature | What It Enables / How It Helps | Impact on Loan Processing & Underwriting |

| Permission-Aware Knowledge Access | Ensures that only authorized users see certain documents or insights. Helps banks maintain confidentiality, regulatory compliance, and reduces risk of over-exposure of sensitive data. | Quicker, secure access to needed data without extra compliance bottlenecks. Underwriters can trust the system to show only what they’re allowed to see, reducing delays for compliance reviews and eliminating manual permission checks. |

| Flexible Deployment Options | Ensures secure, resilient operations across major cloud providers (AWS, Azure & GCP) within your virtual private cloud, or in your on-premise server. | Guarantees strict data residency, security, or regulatory requirements. Reduces friction and allows institutions to adopt DeepQ without compromising existing security or legal constraints, a major barrier for many banks. |

| Contextual Intelligence for Queries | Understands the context of the conversation, and also maintains domain-aware intelligence that helps assist the underwriters regarding domain specific tasks. | Dramatic reduction in time spent by staff manually correlating info across different docs. Faster detection of risky or missing elements. Enables “intelligently summarizing risk” so underwriters get decision-ready insights, not raw unread data. |

| Plug-and-Play Enterprise Integration | Plugs into existing systems quickly, supporting seamless integration with enterprise tools and systems. | Short onboarding time. Banks don’t need to rip out existing systems. Can begin with one loan product or department, prove value and scale. |

Call to Action: What Banks Should Do Next

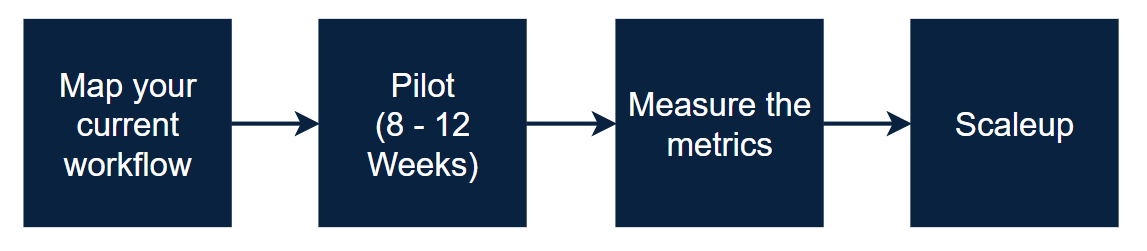

- Map your current workflow and bottlenecks: Identify how loan officers/underwriters handle the loan workflows in your bank and spot the pain points.

- Pilot DeepQ in one product line: For instance, consumer loans or small business underwriting, where document volumes are manageable and regulatory risk is lower.

- Measure the metrics: Time saved, error reduction, customer satisfaction.

- Scaleup: Once the pilot shows strong ROI, adapt it as the business as usual.

Conclusion

In a world where loan applicants expect speed, transparency, and accuracy, financial institutions must evolve or risk falling behind. DeepQ offers a transformational opportunity: to reduce loan review times by 70-80%, move from days or weeks to hours or same-day decisions, while controlling risk and maintaining compliance.

For banks serious about competing in the modern lending era, DeepQ isn’t just nice to have – it’s essential.